Bulletin Search

Disciplinary Actions

JORGE JOSE TIPIANA (Garner) – Following a hearing, The Commission permanently revoked the broker license of Jorge Jose Tipiana effective February 4, 2020. The Commission found that Mr. Tipiana, as the seller of a property he renovated, collected $4000 in due diligence fees from five failed transactions in which Mr. Tipiana repeatedly failed to disclose material facts, including an unpermitted deck, open permits for mechanical and electrical changes, and a sagging structural beam.

JOHNNY E PRATHER (Murphy) – By Consent, the Commission reprimanded Mr. Prather effective March 10, 2020. The Commission found that Mr. Prather served as the broker-in-charge for a firm where one of its brokers advertised a residential property as having 3,264 square feet. This included a garage area and a “safe room” which were not heated by permanently installed conventional heating systems. Mr. Prather also failed to retain records of sketches, calculations, or other documentation that was used in reliance upon the advertised square footage.

WESTERN CAROLINA REAL ESTATE COMPANY INC. (Murphy) – By Consent, the Commission reprimanded Western Carolina Real Estate Company Inc. effective March 10, 2020. The Commission found that one of the firm’s brokers advertised a residential property as having 3,264 square feet. This included a garage area and a “safe room” which were not heated by permanently installed conventional heating systems. The Firm also failed to retain records of sketches, calculations, or other documentation that was used in reliance upon the advertised square footage.

NICKY ARNOLD GUTHRIE (Murphy) – By consent, the Commission suspended the broker license of Mr. Guthrie for a period of 12 months, effective March 10, 2020. The Commission then stayed the suspension for a probationary period through March 10, 2021. The Commission found that Mr. Guthrie listed a residential property for sale and advertised it as having 3,264 square feet. This included a garage area and a “safe room” which were not heated by permanently installed conventional heating systems. He also failed to retain records of sketches, calculations, or other documentation that he relied upon in determining the square footage and relied on the property tax card.

CARINA SCHOENING WOOLRICH (Murphy) – By Consent, the Commission reprimanded Ms. Woolrich effective March 10, 2020. The Commission found that Ms. Woolrich acted as a buyer agent in a residential transaction where the subject property was advertised as having 3,264 square feet. Ms. Woolrich, while informing her buyer clients that she believed the square footage being advertised wrongfully included 576 square feet for a garage, failed to suggest to her clients that they have the property professionally measured to determine the actual square footage. Ms. Woolrich also failed to inform the listing agent of the misrepresentation, a best practice standard, as defined under the Commission’s Residential Square Footage Guidelines.

EDWIN LLOYD MATTHIS JR. (Clinton) – By Consent, the Commission suspended the broker license of Mr. Matthis Jr. for a period of 1 year effective December 1, 2019. In February 2019, Mr. Matthis Jr. self-reported a Misdemeanor Assault on a female conviction more than 60 days following his conviction. He also failed to report two additional convictions, a Misdemeanor Simple Assault from February 2017 and a misdemeanor DV Protective Order Violation from June 2017. Mr. Matthis Jr. also failed to respond to multiple Letters of Inquiry.

STEPHANIE RAY ANSON (Raleigh) – By consent, the Commission suspended the broker license of Ms. Anson for a period of 12 months, effective March 10, 2020. The Commission then stayed the suspension in its entirety. The Commission found that Ms. Anson’s firm listed a residential property for sale and, after going under contract, she received the Home Inspection report, termite report, and repair request via email from the buyer’s agent. Ms. Anson failed to review the documents or go over them with her principal. The termite report noted the presence of subterranean termites with no control measures having been performed along with damaged wood in the crawlspace. The home inspection revealed electrical, plumbing, and structural issues. Soon after the buyer terminated the contract, the subject property went under contract with a subsequent buyer. Ms. Anson failed to disclose the material facts noted in the above reports to this buyer or their agent upon receiving the offer. This buyer terminated the contract after his termite inspection found “extensive termite activity and damage”. Ms. Anson then listed a different residential property for sale and advertised it as a 3-bedroom home as having natural gas heat and being connected to city sewer. After closing, the buyer discovered that the property was on a septic system, which was permitted for two bedrooms, and had propane heat. The seller assisted the buyer in connecting the home to city sewer and the buyer has also converted the heat system to gas.

MEREDITH ANN LUNDBERG (Raleigh) – By consent, the Commission suspended the broker license of Ms. Lundberg for a period of 6 months, effective March 10, 2020. The Commission then stayed the suspension in its entirety. The Commission found that Ms. Lundberg’s firm listed a residential property for sale and, after going under contract, she received the Home Inspection report, termite report, and repair request via email from the buyer’s agent. She forwarded the information to her seller client, but failed to review the documents or go over them with her principal. The termite report noted the presence of subterranean termites with no control measures having been performed along with damaged wood in the crawlspace. The home inspection revealed electrical, plumbing, and structural issues. Soon after the buyer terminated the contract, the subject property went under contract with a subsequent buyer. Ms. Lundberg failed to disclose the material facts noted in the above reports to this buyer or their agent upon receiving the offer. This buyer terminated the contract after his termite inspection found “extensive termite activity and damage”.

KEVIN DESHAWN MORGAN (Durham) – By consent, the Commission suspended the broker license of Mr. Morgan for a period of 2 years, effective August 1, 2019. The Commission then stayed the remaining 1 year after a 1 year active suspension period, effective August 1, 2020. The Commission found that in September 2018, Mr. Morgan, acting as a buyer agent, falsified the signatures and initials of the buyers he represented on an “Exclusive Buyer Agency Agreement”, “Working with Real Estate Agents” brochure, and an “Offer To Purchase and Contract” in a residential sales transaction. Mr. Morgan conducted this real estate transaction with an inactive license after receiving notice from the Commission and a warning from his broker-in-charge, and failed to provide the transaction documents to his firm.

JANE ELLEN GOEBEL (Murphy) – By Consent, the Commission reprimanded Ms. Goebel effective June 3, 2020. The Commission found that Ms. Goebel acted as a buyer agent in a residential purchase transaction. She failed to forward the property disclosure form for the subject property to her buyer clients until after the due diligence period expired. The seller indicated on the disclosure form that the subject property was located on a private road/street and that no maintenance agreement existed. The buyers terminated the contract when they discovered that they would be responsible for the maintenance of the private road/street.

MAXWELL LOUIS GOEBEL (Murphy) – By Consent, the Commission reprimanded Mr. Goebel effective June 3, 2020. The Commission found that Mr. Goebel acted as a buyer agent in a residential purchase transaction. He failed to forward the property disclosure form for the subject property to his buyer clients until after the due diligence period expired. The seller indicated on the disclosure form that the subject property was located on a private road/street and that no maintenance agreement existed. The buyers terminated the contract when they discovered that they would be responsible for the maintenance of the private road/street.

Appearances

Jean Hobbs, Auditor/Investigator, recently spoke at Allen Tate’s business meeting in Charlotte NC.

Nick Smith, Consumer Protection Officer, recently spoke at Keller Williams of Greensboro’s Time Out Tuesday Series in Greensboro NC.

Marcia Waldron, Auditor, recently spoke at Greensboro Landlord Association in Greensboro NC.

Mary Wills Bode has been appointed to the Commission

Mary Wills Bode of Raleigh has been appointed by Governor Roy Cooper to the North Carolina Real Estate Commission for a term ending July 21, 2022, announced Miriam J. Baer, Executive Director.

Mary Wills Bode of Raleigh has been appointed by Governor Roy Cooper to the North Carolina Real Estate Commission for the term ending July 21, 2022, announced Miriam J. Baer, Executive Director.

Bode is the Executive Director of North Carolinians for Redistricting Reform (NC4RR) in Raleigh, a bipartisan non-profit co-chaired by Tom Ross and Rep. Chuck McGrady that seeks to improve representative democracy through redistricting reform.

Prior to her role with NC4RR, Bode was a corporate attorney at Proskauer Rose LLP and Cahill Gordon & Reindel LLP in New York, where she specialized in capital markets, leveraged finance, as well as mergers and acquisitions.

While in law school, Bode worked for the Office of the Federal Public Defender for the Eastern District of North Carolina (EDNC), The Honorable U.S. Magistrate Judge William Webb, U.S. District Court, EDNC in Raleigh, North Carolina, as well as The Honorable Senior District Judge Malcolm Howard, U.S. District Court, EDNC in Greenville, North Carolina.

She was honored with The American Lawyer’s M&A Global Deal of the Year for her cross-border legal work in Europe in 2016. Bode holds a Juris Doctorate from the University of North Carolina at Chapel Hill, where she was a member of the North Carolina Law Review, and Bachelor of Arts degree in Economics and Psychology from Wake Forest University.

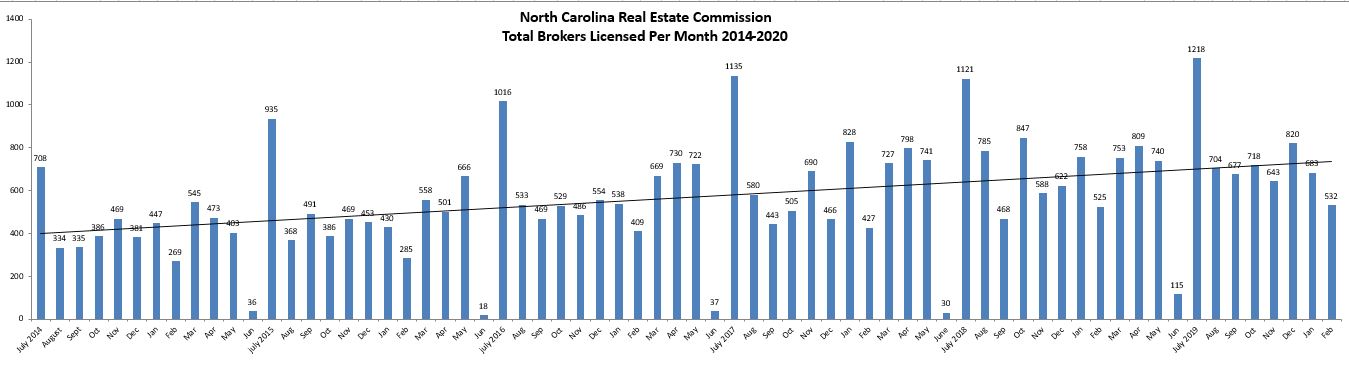

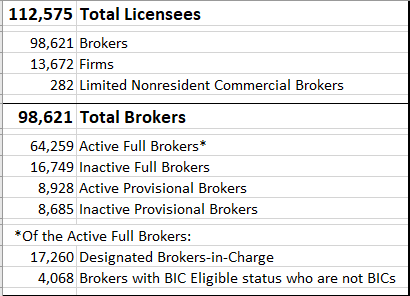

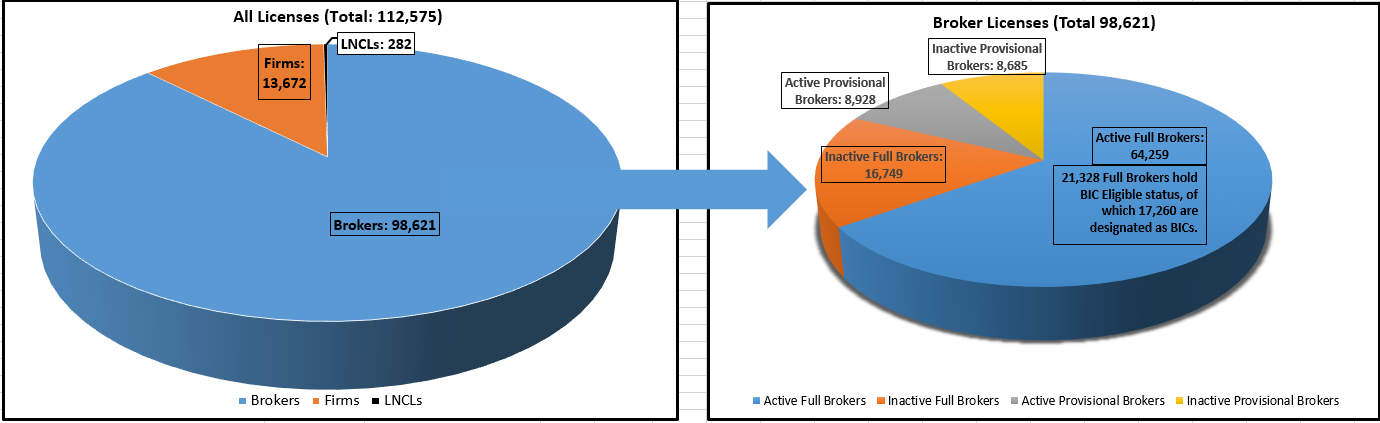

Current Stats: Brokers Licensed per Month

Disciplinary Actions

ALI KHALESEH DEHGHAN (Eastern NC) – By Consent, the Commission suspended the broker license of Mr. Dehghan for a period of 2 years effective February 12, 2020. The Commission then stayed the suspension adding that the stayed suspension shall be terminated at such time as Mr. Dehghan is no longer on supervised probation. The Commission found that in December 2018, Mr. Dehghan was indicted in the US District Court, Eastern Division of NC, for knowingly possessing a firearm in violation of 18 UC 922(g)(5)(A) and 924. Mr. Dehghan pleaded guilty and was ordered to serve 6 months in prison, given credit for time served, and placed on supervised probation for 3 years.

PAUL EMANUEL JONES (Wilmington) – By Consent, the Commission reprimanded Mr. Jones effective February 12, 2020. The Commission found that in June 2019, Mr. Jones while attending a GENUP course, was disruptive to the point of being removed from the class.

KIMBERLY ANNE SARNO (Carthage) – The Commission accepted the permanent voluntary surrender of the broker license of Ms. Sarno effective February 12, 2020. The Commission dismissed without prejudice allegations that Ms. Sarno violated provisions of the Real Estate License Law and Commission rules. Ms. Sarno neither admitted nor denied misconduct.

WILLIAM B CHALK JR. (Morehead City) – By Consent, the Commission reprimanded Mr. Chalk Jr. effective March 10, 2020. The Commission found that Mr. Chalk served as the broker-in-charge for a firm and that on or about December 2017, a Property Management Agreement was executed by the owner of the residential property, and an unlicensed employee, who handled all aspects of the management of the subject property, despite not being licensed. The firm deducted repair expenses from the owner’s proceeds, despite the lease requiring the tenant to be responsible for those repairs. The Lease Addendum, created by the unlicensed employee, required the tenant to make extensive repairs to the subject property in exchange for a reduced monthly rental payment.

CHALK & GIBBS INC. (Morehead City) – By Consent, the Commission reprimanded Chalk & Gibbs Inc. effective March 10, 2020. The Commission found that on or about December 2017, a Property Management Agreement was executed by the owner of the residential property, and an unlicensed employee, who handled all aspects of the management of the subject property, despite not being licensed. The firm deducted repair expenses from the owner’s proceeds, despite the lease requiring the tenant to be responsible for those repairs. The Lease Addendum, created by the unlicensed employee, required the tenant to make extensive repairs to the subject property in exchange for a reduced monthly rental payment.

Q MAXWELL ERNEST GILLAND (Charlotte) – By Consent, the Commission reprimanded the broker license of Mr. Gilland effective February 1, 2020. The Commission found that in 2017, Mr. Gilland, a provisional broker, referred a seller-client to his firm after learning confidential information about the seller-client. Subsequently, Mr. Gilland represented a buyer-client in a transaction with the firm’s seller-client. Mr. Gilland promised his buyer-client $5,000 to help the transaction close and issued a check for $5,000, but stopped payment on the check and failed to ever pay his buyer-client.

STACY SECHREST PRANGER (High Point) – By Consent, the Commission reprimanded Ms. Pranger effective February 10, 2020 on certain conditions. The Commission found that Ms. Pranger, a broker-in-charge, failed to maintain her firm’s trust account records in compliance with Commission rules including failure to perform reconciliations, failure to do trial balances, failure to include required information on checks and deposits, and failure to accurately input expenses and deposits. Ms. Pranger also charged for services when fees were not clearly listed in the property management agreement. The Commission notes that Ms. Pranger and her firm are now in substantial compliance with Commission rules.

GATE CITY PROPERTY MANAGEMENT LLC (High Point) – By Consent, the Commission reprimanded Gate City Property Management LLC effective February 10, 2020, on certain conditions. The Commission found that the firm failed to maintain its trust account records in compliance with Commission rules including failure to perform reconciliations, failure to do trial balances, failure to include required information on checks and deposits, and failure to accurately input expenses and deposits. The firm also charged for services when fees were not clearly listed in the property management agreement. The Commission notes that the firm is now in substantial compliance with Commission rules.

GREGORY A FAULCON (Charlotte) – By Consent, the Commission reprimanded Mr. Faulcon effective April 1, 2020. The Commission found that in April 2018, Mr. Faulcon listed a HUD foreclosure property and represented the property in the MLS as a three-bedroom mobile home. Mr. Faulcon did not obtain or review a copy of the septic permit, which indicated that the septic system was designed for two bedrooms. A buyer purchased the property with the understanding that it was a three-bedroom mobile home. Mr. Faulcon has since paid the buyer the cost to upgrade to a three bedroom system.

FAULCON & ASSOCIATES REAL ESTATE LLC (Charlotte) – By Consent, the Commission reprimanded Faulcon & Associates Real Estate LLC effective April 1, 2020. The Commission found that in April 2018, Faulcon & Associates Real Estate LLC listed a HUD foreclosure property and represented the property in the MLS as a three-bedroom mobile home. The firm did not obtain or review a copy of the septic permit, which indicated that the septic system was designed for two bedrooms. A buyer purchased the property with the understanding that it was a three-bedroom mobile home. The buyer later discovered the misrepresentation when selling the property when his listing agent obtained the septic permit as part of the listing process. The firm has since paid the buyer the cost to upgrade to a three bedroom system.

How to apply for a Firm License

Have you created an LLC, corporation, partnership, or other type of business entity for your brokerage business or compensation? If so, you need to apply for a firm license.

To complete a firm license application, you must:

- provide the registered legal and assumed name(s) for the entity;

- provide the SOSID assigned by the NC Secretary of State (not applicable for partnerships);

- provide physical and mailing addresses for all office locations;

- designate a Qualifying Broker (QB)*; and

- designate a Broker-in-Charge (BIC) for each office location.

*Commission Rule 58A .0502 dictates that a firm must have one principal who holds a broker license on active status in good standing; that broker must serve as the qualifying broker (QB). The QB is responsible for:

- designating and assuring that there is a BIC for each office location;

- renewing the real estate broker license of the entity each license year;

- retaining the firm’s pocket card at the firm;

- notifying the Commission of any change of business address or legal or trade name of the entity:

- notifying the Commission in their change of status as qualifying broker;

- securing and preserving the transaction and trust account records of the firm whenever there is a change in the broker-in-charge;

- retaining and preserving the transaction and trust account records of the firm upon their termination as qualifying broker;

- notifying the commission if, upon their termination of his or her status as qualifying broker, the firms transaction or trust account records cannot be retained or preserved; and

- notifying the Commission regarding any revenue suspension, revocation of authority, or administrative dissolution.

To apply for a firm license, go to www.ncrec.gov and click on Apply for a Firm License.

If you have further questions about the firm licensing process, contact the Education and Licensing Division at 919.875.3700.

Postlicensing Education Deadline

This article from the February eBulletin is republished here to remind brokers of the new Postlicensing Education requirement effective July 1, 2020.

Beginning July 1, 2020, Rule 58A .1902 will require a Provisional Broker to complete all three 30-hour Postlicensing courses within 18 months of initial licensure in order to maintain active license status.

If you were licensed anytime during 2018, you must complete all your Postlicensing courses by July 1, 2020. If you have been licensed in 2019, you will have at least 18 months from your date of licensure to complete the courses.

Example #1: Licensed on February 1, 2018

- 1st Postlicensing course deadline: February 1, 2019

- 2nd Postlicensing course deadline: February 1, 2020

- 3rd Postlicensing course deadline: June 30, 2020

Example #2: Licensed on March 17, 2019

- 1st Postlicensing course deadline: March 17, 2020

- 2nd & 3rd Postlicensing course deadlines: September 17, 2020

Additional information about this important change is provided in the General Update (GENUP) and Broker-in-Charge (BICUP) courses throughout the year. Also, if you are a provisional broker, be on the lookout for email communications from the Commission about the changing education deadlines.

If you have further questions regarding this rule change, please contact the Education and Licensing Division at 919.875.3700.

Self-Dealing

A Regulatory Affairs Case Study

By Rob Patchett

As fiduciaries, brokers are required to place their clients’ interests above their own interests. This also means that brokers are prohibited from engaging in self-dealing. In one case, a broker went to great lengths to attempt to purchase a condominium from her client at well below market value.

Respondent Broker was the qualifying broker and broker-in-charge of her solo firm. Her husband’s lease on a condominium was approaching its termination and the owner contacted Respondent Broker and her husband to see if they would purchase the condo at the end of the tenancy. Respondent Broker and her husband decided not to purchase the condominium, but Respondent Broker offered to list the condo for the owner. Respondent Broker represented to the owner-seller she knew investors who were interested in purchasing a condominium. The owner-seller and Respondent Broker executed a six-month exclusive listing agreement with a 5% commission at a list price of $226,000.

After several weeks, Respondent Broker informed her seller-client that the potential investors were not interested in making an offer on the condominium, but her husband had renewed interest in purchasing the condominium. The seller-client spoke directly to Respondent Broker’s husband who offered $215,000 to purchase the condominium; the seller rejected his offer. At this time, Respondent Broker had never publically advertised the condominium for sale.

Suspicious, the seller spoke to another broker about the sale of his condominium. This broker was shocked to hear the list price was so low. He informed the seller that his condominium should be listed between $250,000 and $270,000 based upon recent sales. After learning this information, the seller-client emailed Respondent Broker asking to terminate the listing agreement. The broker refused to terminate the agreement.

A few weeks later, Respondent Broker emailed her seller-client a letter purportedly from Respondent Broker’s attorney. The letter demanded the seller-client accept the husband’s offer because it was a “full-price” offer. The seller-client was given two options for accepting the offer. He could sell the condominium to the husband for $215,000 and not pay Respondent Broker a commission or sell the condominium for $226,000 and pay a 5% commission. The letter was unsigned and contained several factual and typographical errors. During the course of the Commission’s investigation, the Commission’s Consumer Protection Officer confirmed that the attorney did not draft, sign, or send the letter to the seller. Evidence tends to indicate that either Respondent Broker or her husband drafted the letter purporting to be an attorney.

The seller-client rejected all of the husband’s offers. Respondent Broker then demanded her seller-client pay her commission for bringing a “ready, willing, and able buyer” that he rejected. The seller-client declined to pay Respondent Broker’s commission. Several months later, the seller-client sold his condominium for $269,000.

In this case, Respondent Broker’s only concern was for her personal gain. She attempted to buy her client’s condominium below market value by misrepresenting the fair market value to her client. She also attempted to force her seller-client into selling by sending a fictitious attorney demand letter. Finally, she attempted to collect a commission by claiming she brought a legitimate “ready, willing, and able buyer” to her seller-client. Following the investigation, the broker surrendered her license and that of her firm.

Brokers owe fiduciary duties to their clients. These fiduciary duties prohibit brokers from self-dealing. Commission rule 58A .0104(p) specifically requires listing brokers to disclose in writing conflicts of interest, transfer or terminate listing agreements, and notify the seller-client that they may terminate the listing agreement prior to entering into a contract for a property that the listing broker or firm is listing. Furthermore, North Carolina General Statute 93A-6(a)(8) and (10) gives the Commission authority to discipline brokers who are unworthy or incompetent to act as real estate brokers in a manner as to endanger the interest of the public and for conduct which constitutes improper, fraudulent, or dishonest dealing, respectively.

“When Personal Property Disappears …”

A Regulatory Affairs Case Study

By Danielle M. Alston, Consumer Protection Auditor

The complaining witness in this case was a seller whose home was listed by an agent. The Respondents were a provisional broker acting as a buyer agent and her Broker-in-Charge (BIC).

The Buyer Agent scheduled a showing of the subject property and the Seller approved it. Shortly after the showing, the Seller contacted the Buyer Agent very upset, alleging that the buyers had taken some prescription medications that were “well hidden” in the Seller’s master bathroom.

During the investigation, the Buyer Agent stated she was contacted by a woman through social media expressing her interest in seeing the property with her husband. The Buyer Agent stated that she met the couple at the property as opposed to her normal practice of meeting prospective buyers at her office or a public place prior to showing the home. She explained that the opportunity of getting a badly-needed client outweighed her usual, more cautious approach. Upon arriving at the property, the Buyer Agent said she reviewed the “Working With Real Estate Agents” brochure with the couple, who stated that they would sign it after the showing was complete. The Buyer Agent did not check the buyers IDs or even get their names.

When she was showing the first-floor master bedroom, the buyer-wife indicated that she needed to use the bathroom. The Buyer Agent planned to wait for the wife to exit the bathroom, but the husband began walking out of the master bedroom while asking questions, so the Buyer Agent followed him to answer his questions. The husband inquired about the upstairs, so the Buyer Agent showed the upstairs to him while his wife was still in the bathroom. By the time the Buyer Agent came back downstairs with the husband, the wife was in the kitchen and the Buyer Agent heard a cabinet door close. The Buyer Agent indicated that she was not concerned as buyers typically inspect cabinets.

The Buyer Agent indicated that she attempted to ask the couple several follow-up questions as they began to leave. The wife wrote down a contact number at the request of the Respondent Broker and then left without signing the “Working With Real Estate Agents” disclosure. The contact number allegedly provided by the buyers was not a valid number.

Later, the Seller called the police and reported the theft of her prescription medication. An officer explained to the Seller that this was a somewhat common scam for two people to pose as interested buyers in order to steal things from a home. The officer also contacted the Buyer Agent that night for her version of the incident.

The evidence in this case tended to show that the unidentified potential buyers were responsible for the Seller’s missing medications. However, the Commission cautioned that Buyer Agent about her conduct, including her failure to identify the prospective buyers before taking them into the Seller’s home.

A few months later, the Buyer Agent changed firms and the Commission subsequently received a call from the Buyer Agent’s new BIC, who explained that she was notified that the Buyer Agent had recently tested positive for opioids. The Commission staff began a new investigation to obtain more information.

The Buyer Agent’s new BIC provided a list of the Buyer Agent’s showings to the Commission staff. Commission staff also received a call from a family member of the Buyer Agent, who explained that the Buyer Agent had been in a medically-assisted drug treatment program for almost two years and that the Buyer Agent had recently tested positive for drugs not prescribed through the treatment program. The family member provided photos of prescription bottles for other individuals found in the Buyer Agent’s home. The Commission also received a video in which the Buyer Agent admitted that she scheduled and conducted false showings to gain access to listed homes in order to steal prescription drugs for her own use. Following the conclusion of the investigation, the Buyer Agent entered into a Consent Order with the Commission in which she voluntarily agreed to surrender her broker license.

This case illustrates the importance of listing agents advising their seller-clients to remove or lock up all prescription medications, cash, jewelry, collections, firearms, and other valuables that can be taken during showings. Sellers who wish to use interior cameras for detection and deterrence of theft should be advised that they cannot use cameras with audio and cannot place a camera in any room/area in which there is a reasonable expectation of privacy, such as a bathroom.